The Slow Leak: Why Sitting in Cash Is a Bet, Not a Safe Choice

Why holding cash quietly costs you, and what people have always done about it

5 min read

The briefing serious investors read first.

Free analysis before markets open. Start thinking in decades, not days.

Join 45,000+ readers · No spam · Unsubscribe anytime

Before we begin: this report is for education, not financial advice. Nothing here is a recommendation to buy or sell any stock, company, or asset, and we make no price predictions. Investing carries risk, including loss. Please read the full disclaimer at the end.

The slow leak in your wallet

Here is a question that sounds simple and is not.

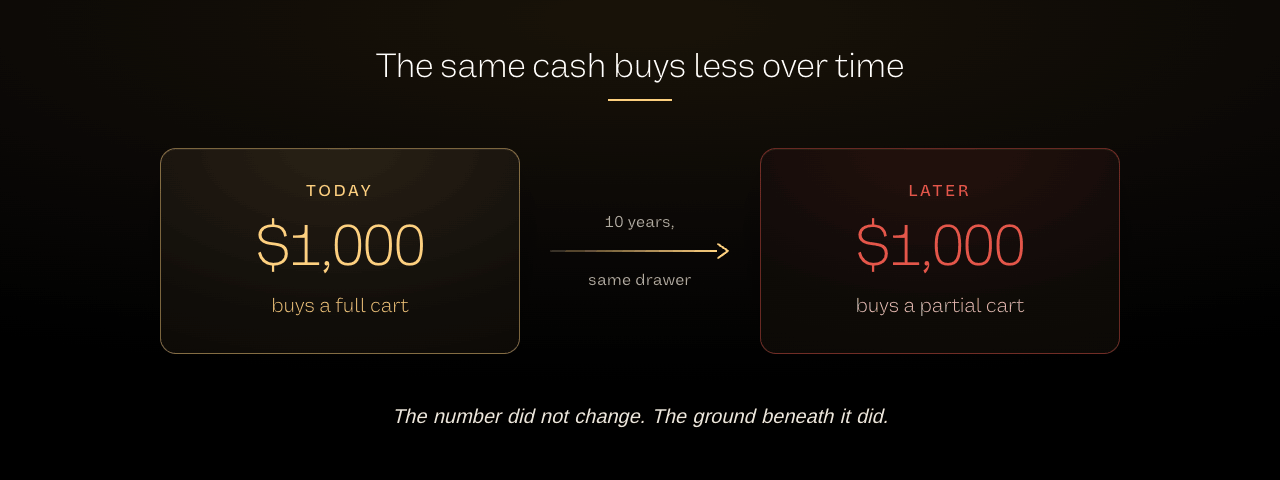

If you put a sum of cash in a drawer and came back in ten years, would you have the same amount of money?

The number on the bills would be identical. But the amount of life that money could buy, the groceries, the rent, the plane tickets, would almost certainly be smaller. Sometimes a little smaller. Sometimes a lot.

Your cash did not move. The ground underneath it did.

This slow leak has a name that sounds technical but describes something very ordinary: debasement. It is the gradual loss of a currency's purchasing power as more of that currency gets created. And over the past couple of decades, the rate of money creation has been one of the defining facts of the financial world.

But here's what everyone is missing in the headlines...

Most people only notice debasement when prices at the shop jump. By then they are feeling the late symptoms. The cause showed up much earlier and much more quietly, in how much money was being created in the first place. Learn to watch the cause, and the whole picture changes. This report explains where debasement comes from, why it is so easy to miss, and what people through history have done to protect the value of what they have saved. None of it is a recommendation. It is the mechanism, and the long, well-documented pattern.

Where new money comes from

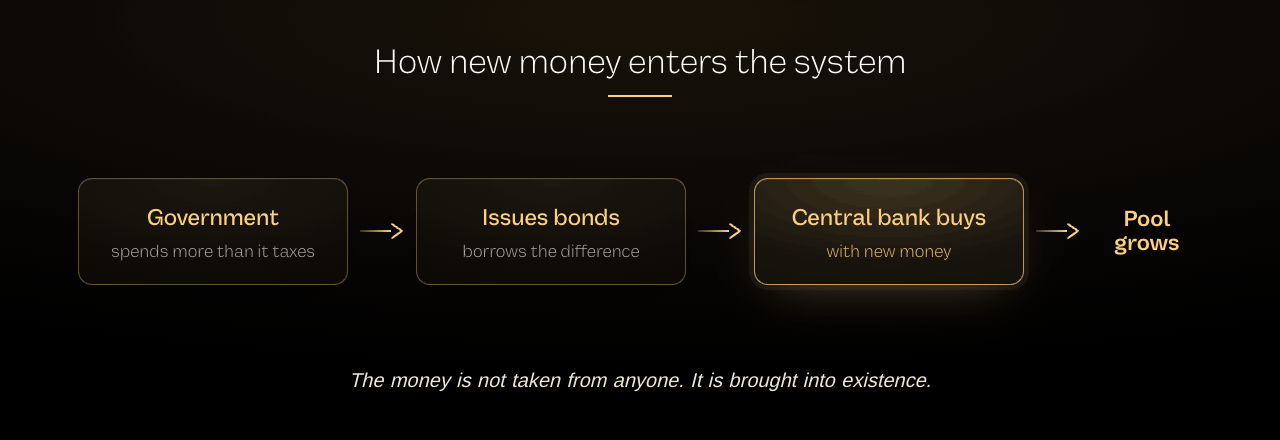

To understand debasement, you have to understand one habit of modern governments.

When a government spends more than it collects in taxes, which is most of the time, it makes up the difference by borrowing. It issues bonds, effectively IOUs, and sells them.

Here is the part that matters. Central banks, like the US Federal Reserve, can step in and buy large amounts of those bonds using newly created money. That money is not taken from anyone. It is brought into existence, electronically, and added to the system. This is how the total pool of money grows. And it has grown a great deal.

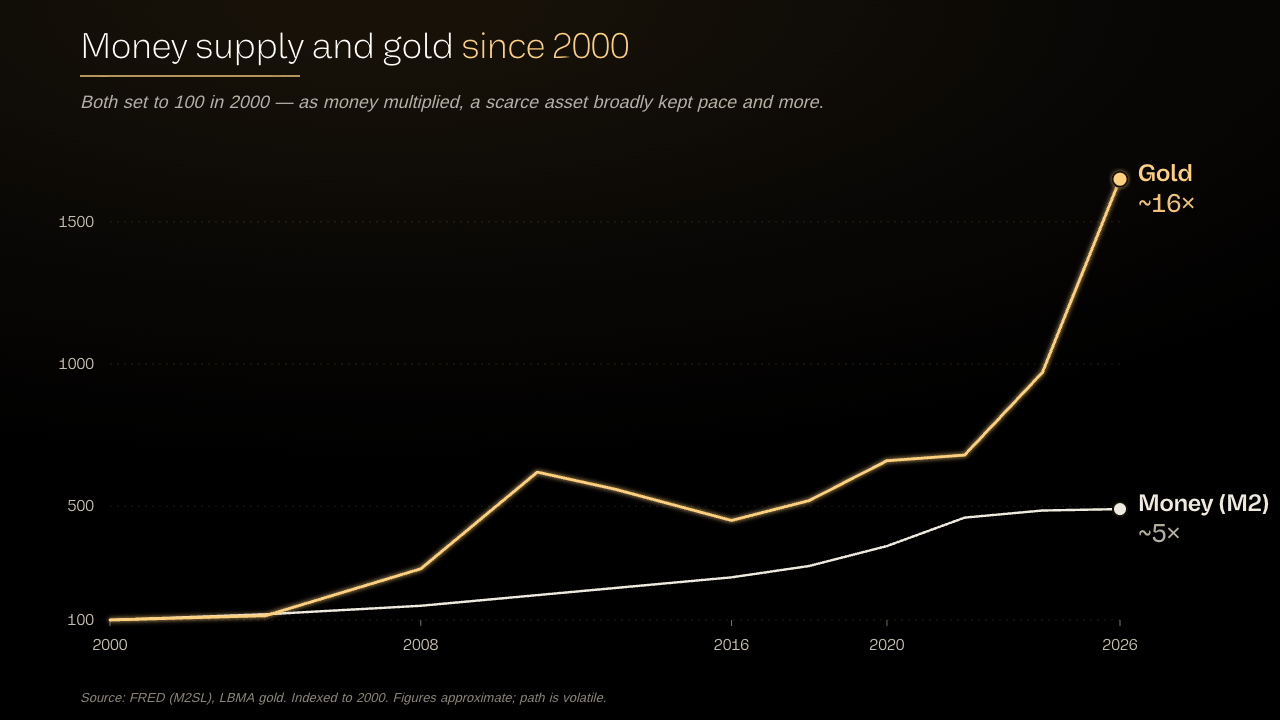

A broad measure of US money, called M2, stood at roughly $4.6 trillion in the year 2000. By 2026 it had climbed to around $22.7 trillion. During the pandemic alone, the pool jumped by a remarkable amount in a very short time, as the Fed created money at a pace rarely seen in peacetime.

More dollars came into being. The dollars already in your drawer did not become fewer. They just became a smaller slice of a much bigger pie.

Why you do not always feel it right away

Here is the sneaky part, and the reason debasement fools so many people.

When new money is created, it does not always show up as higher prices at the supermarket straight away. For long stretches, everyday inflation can look calm even while the money supply balloons.

So where does the effect go first? Often into assets. Things that cannot simply be printed: stocks, property, gold, scarce digital assets. When there is far more money around and not many more of these things, their prices tend to rise.

This is why you can have a period where the cost of bread looks stable, yet house prices and stock markets climb out of reach. The money was being created the whole time. The pressure simply showed up in assets first, and in the shopping bill later.

History has shown this lag can stretch for years before it closes. But the long record suggests it tends to close eventually. The quiet erosion at the monetary level becomes the loud inflation people complain about, often well after the money was created.

The pattern people have leaned on for centuries

So if cash slowly leaks value when money is being created, what have people done about it?

The oldest answer is to hold things that cannot be printed.

The classic example is gold. Its appeal is almost boringly simple: no government can create more of it on a whim. The supply grows slowly and with great effort. So when the supply of money expands quickly and the supply of gold does not, it takes more dollars to buy the same ounce. Often that reflects the measuring stick getting shorter rather than gold itself becoming more valuable.

The long record is striking. Across the same stretch that US money supply multiplied many times over, gold went from a few hundred dollars an ounce around the year 2000 to several thousand by 2026. There were sharp pullbacks and frightening years along the way. The path was never smooth. But the broad direction tracked the expansion of money with remarkable persistence.

Gold is the traditional example, but the principle is broader than any single asset. The underlying idea is scarcity. In a world where the supply of money keeps growing, assets whose supply cannot easily grow have historically held their ground better than cash.

That logic is why some people extend the same thinking to other genuinely scarce things, and why the debate over which assets best preserve value is as old as money itself.

A reminder worth stating plainly here. Has held its value over long periods is a statement about history, not a promise about the future. Every one of these assets can fall hard and stay down for years. Scarcity is a reason something has tended to resist debasement; it is not a guarantee of a smooth ride or a good entry price today.

ABN System

Seeing the leak is step one. Plugging it is step two.

Once you understand that cash erodes as money is printed, the question becomes how to hold wealth in things designed to resist it, without giving up safety or sleep. Our free ABN System training lays out the exact three-part framework we use to do that.

Watch the ABN System training →The tell that the big players watch

You are not the only one thinking about this. Some of the largest, most conservative institutions in the world watch debasement closely, and act on it.

The clearest evidence is central banks themselves. The very institutions that issue currency have, for many years running, been net buyers of gold for their own reserves. Think about what that signals. The people closest to the money-printing machine choose to hold a meaningful slice of their savings in something that cannot be printed.

There is even a rough gauge analysts use to size all this up: comparing the total amount of money in the system against the total value of all the gold in the world. When money grows much faster than the fixed pile of gold, that ratio stretches, and it has been a long-running way of asking whether money has been created faster than hard assets can absorb. You do not need to track that ratio yourself. The point is simpler. When the institutions with the clearest view of money creation consistently hedge against it, that is a tell worth understanding.

How to see debasement for yourself, for free

This is the part you can act on the moment you finish reading. All of this data is public and free.

1. Watch the money supply.

The broad measure, M2, shows the size of the money pool over time. The Federal Reserve Bank of St. Louis publishes it free on its FRED database. Open the M2 money supply chart on FRED. What to look for: the long-term line. It mostly climbs. The question is the pace, is money being created faster or slower lately?

2. Watch the dollar's strength against other currencies.

A gauge called the dollar index measures the dollar against a basket of other major currencies. It is one quick read on confidence in the dollar. Find the US dollar index on FRED. What to look for: a falling dollar can be a sign of debasement pressure relative to other currencies, though it is only one piece of the picture.

3. Compare a scarce asset to the money supply over time.

Pull up a long-term chart of gold, or another scarce asset you are curious about, and mentally lay it next to the M2 chart. You are looking for whether the scarce thing has roughly kept pace with money creation over long periods. What to look for: not a perfect match, the path is always bumpy, but the broad relationship over decades.

4. Notice your own prices.

The most personal gauge of all. Keep a rough mental note of what your regular purchases cost over the years, your groceries, your rent, a coffee. That lived experience is debasement made tangible, and it keeps the abstract numbers honest.

A note on expectations, so you use this well. Watching debasement tells you about a long, slow force, not next month's move. Scarce assets can and do fall sharply over months or even years. This is a lens for understanding why holding only cash carries a hidden cost over long stretches, not a signal to pile into any particular asset at any particular price.

The balance most people miss

None of this means cash is useless. Far from it.

Cash is safety. It is the money you need on hand for emergencies, for opportunities, for sleeping at night. Everyone needs some, and trying to be fully invested at all times is its own kind of mistake.

The insight is subtler. It is that holding only cash, over long periods, quietly costs you purchasing power in an era of persistent money creation. The leak is slow enough to ignore day to day, and real enough to matter over a decade.

So the question debasement raises is not cash or no cash. It is about balance: how much you keep liquid and safe, and how much you hold in things designed to resist the leak. That balance is deeply personal, and it depends on your goals, your timeline, and how much volatility you can stomach. There is no single right answer, and anyone who offers you one without knowing your situation should be treated with caution.

The one idea to take with you

If you forget everything else, keep this.

The number on your cash does not change, but the ground beneath it can. In an era where money is created faster than scarce things can be made, sitting entirely in cash is not the safe, neutral choice it feels like. It is a slow, quiet bet that the leak will not matter.

For centuries, people who understood this have kept a portion of their savings in things that cannot be printed. They did it to hedge against the erosion they could see coming in the money itself, not to gamble.

You can now watch that same erosion, for free, in a browser. That alone puts you ahead of most savers, who never see the leak until the prices catch up.

- Rami Al-Sabeq (Editor in Chief | Future Finance)

About Future Finance

Future Finance is written by Rami Al-Sabeq, Editor-in-Chief, and his research team. His macro-to-crypto work has been featured in Unchained and Cryptonary, and his independent essays appear at RamiWrites.Substack.com.

Behind every issue sits Head of Research Tyler Hubbard, whose track record across 590+ digital asset picks has produced an 85% directional accuracy rate and a 426% average peak return. That's as of the third-party audit measuring performance through April 30th, 2026. Follow him on TradingView here.

Free Strategy Call

Where to go from here

The leak is personal. So is the fix. How much to keep liquid and how much to hold in scarce assets depends entirely on your situation. On a free strategy call, we'll talk through how the debasement lens applies to your savings, timeline, and comfort with risk, no jargon, no obligation.

Book your free strategy call →Disclaimer: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. Future Finance is not a registered financial advisor or broker-dealer. The data sources and tools referenced are provided for independent research and are not endorsements. All investments carry risk, including the possible loss of the entire amount invested. Assets described as historical stores of value, including gold and other scarce assets, can and do decline significantly in price and may underperform for extended periods; past performance is not indicative of future results, and historical patterns described here may not repeat. Holding cash also carries risk, including the erosion of purchasing power. The financial figures cited are approximate and accurate only as of mid-2026; they change constantly, so verify all current data independently using the linked sources. Markets can move against you, and you should never invest money you cannot afford to lose. Always conduct your own research and consult a qualified, licensed financial advisor who understands your personal circumstances before making any investment decision.

Editor's Pick

Become a sharper capital allocator in 5 minutes a day.

Institutional-grade research on where the smartest capital is positioning, across AI, energy, biotech, robotics, and digital assets. Distilled into a daily read you finish before your coffee does.

Join 45,000+ readers · No spam · Unsubscribe anytime