The $200 Billion Financial System That Runs Without a Single Banker

What it really means to hold and grow money without a bank in the middle

6 min read

The briefing serious investors read first.

Free analysis before markets open. Start thinking in decades, not days.

Join 45,000+ readers · No spam · Unsubscribe anytime

The question hiding inside your bank account

Think about what a bank actually does for you.

It holds your money. It moves it when you ask. It pays you a little interest on your savings, lends your deposits to other people, and lets you borrow when you need to. It keeps a ledger of who owns what, and it stands between you and your money as the trusted middleman for all of it.

For most of modern history, there was no alternative. If you wanted those services, you needed an institution to provide them, and you needed to trust that institution to stay solvent, to follow the rules, and to give you your money back when you asked.

A new set of tools quietly changes that arrangement. They are known collectively as decentralized finance, or DeFi, and the phrase that captures the whole idea is become your own bank.

But here's what everyone is missing in the headlines...

Become your own bank is usually sold as pure freedom, and the freedom is real. What gets glossed over is the other half: a bank does a great deal of unglamorous, protective work on your behalf, and when you remove the bank, that work does not disappear. It lands on you. This report explains honestly what DeFi lets you do, how it works underneath, and what you take on when there is no institution standing between you and your money. None of it is a recommendation. It is the picture, both halves of it.

What DeFi actually is

Strip away the jargon and DeFi is a simple idea with a powerful twist.

It is a set of financial services, holding money, earning interest, lending, borrowing, trading, that run on a public blockchain instead of inside a company. The services are delivered not by employees and account managers but by smart contracts: programs that live on the blockchain and execute their rules automatically, exactly as written, for anyone who interacts with them.

A useful way to picture a smart contract is as a vending machine. A vending machine does not need a shopkeeper. You put money in, you make a selection, and the machine releases your snack according to fixed rules that everyone can see. There is no manager to ask permission, no closing time, and no discretion about whether you qualify. The machine simply does what it was built to do. A smart contract is a vending machine for financial services.

Because these services run on open code rather than inside an institution, they have a few unusual properties. They are available to anyone with an internet connection and a crypto wallet, with no application and no approval. They run constantly, every hour of every day, with no weekends or banking holidays. And the rules are visible to everyone, written in code that anyone can inspect.

The scale is no longer trivial. Tens of billions of dollars sit inside these protocols, and the digital dollars that move through them, the stablecoins we will come to shortly, represent a market in the hundreds of billions. This is a real, functioning financial system, even if it remains far smaller than the traditional one. For now, at least.

The keys, the wallet, and what self-custody means

Before the services make sense, you need the one concept that sits at the heart of become your own bank.

In the traditional world, the bank holds your money and you hold a claim on it. Your name in their database is what entitles you to your funds. If you lose your password, you call them and prove who you are, and they restore your access. The bank is the ultimate keeper of your account.

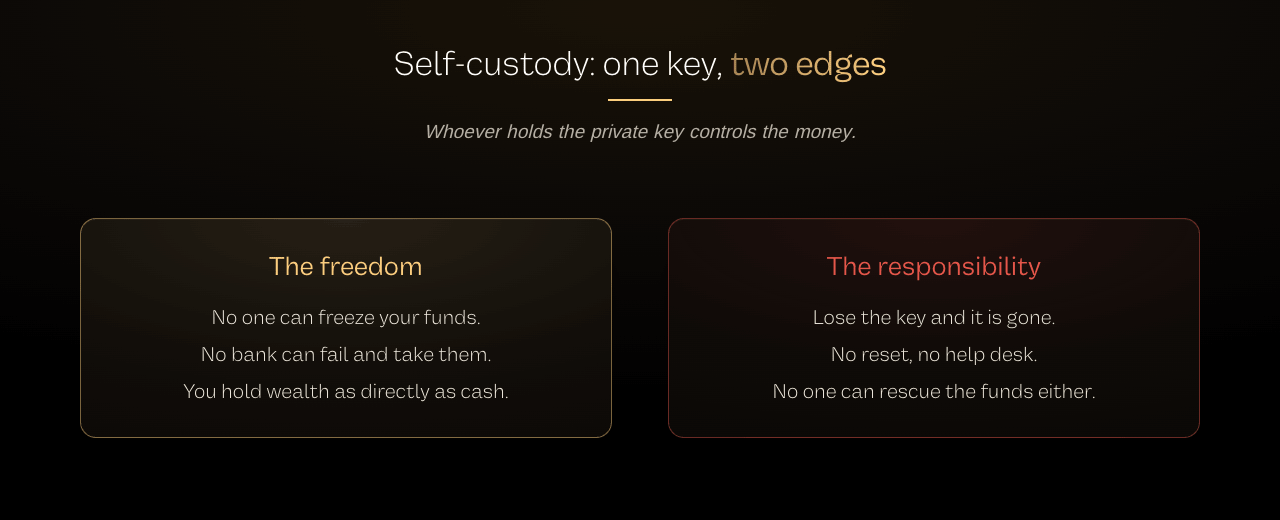

In DeFi, you hold your money directly, through something called a wallet. A crypto wallet does not actually store your coins; the coins live on the blockchain. What the wallet stores is a secret, called a private key, that proves the coins are yours and lets you move them. Whoever holds the private key controls the money, completely and without exception.

This is called self-custody, and it is the core trade-off of the entire space.

The upside is genuine and profound. No bank can freeze your account, block a payment, or fail and take your savings down with it. You are not trusting an institution to stay solvent. You hold your wealth as directly as if it were cash in your own hand, but it can travel the world in minutes.

The downside is equally real, and it is where people get hurt. If you lose your private key, there is no help desk to call and no password reset. The money is simply gone, permanently. If someone tricks you into revealing that key, they can empty your wallet and nothing can reverse it. The same property that means no one can freeze your funds also means no one can rescue them. You are the keeper of the account now, with all the power and all the responsibility that implies.

Becoming your own bank starts here. You gain total control, and you accept total responsibility for the keys.

What you can actually do: saving and earning

Once you hold your own funds, the services begin to look like a bank's, with the middleman replaced by code.

Start with the most familiar: earning interest on savings. In DeFi, you can deposit funds into a lending service, and other users borrow them and pay interest, a share of which flows to you. We covered the key point in our report on real versus inflationary yield: durable interest comes from real borrowing demand, rather than from a project printing tokens to lure you in. The mechanism is the same one a bank uses when it lends out your deposits, except here you can see the whole thing happening on-chain, and you are dealing with code rather than a branch.

To make this work, DeFi needs a kind of money that does not swing wildly in value, because nobody wants their savings or their loan denominated in something that can drop 20% in a day. That is the job of the stablecoin.

A stablecoin is a digital token designed to hold a steady value, almost always one US dollar. It is the unit of account that makes the whole system usable: loans, interest, and trades are measured in these steady digital dollars rather than in volatile coins. The largest stablecoins represent hundreds of billions of dollars between them, and they are the quiet backbone that lets DeFi behave like a financial system rather than a casino. They are not without their own risks, which we will get to, but they are what makes earning interest on dollars, on-chain possible at all.

What you can actually do: borrowing without permission

The other side of a bank is borrowing, and here DeFi works in a way that surprises almost everyone the first time.

When you borrow from a bank, the bank checks your credit, verifies your identity, and decides whether to trust you. In DeFi, there is no credit check and no identity at all. So how can a faceless smart contract safely lend you money?

The answer is collateral, and specifically, more collateral than you borrow. This is called over-collateralization, and it is the clever trick that makes trustless borrowing possible.

In practice it works like this. To borrow, say, $100 worth of stablecoins, you first lock up something more valuable, perhaps $150 worth of another crypto asset, as collateral. The smart contract holds your collateral and hands you the loan. As long as your collateral stays comfortably above your loan, everything is fine, and you can repay whenever you like to unlock it.

Why would anyone post $150 to borrow $100? Because it lets you borrow against assets you do not want to sell, without asking anyone's permission, in minutes, with no paperwork. Someone who holds crypto they believe in long term can borrow stable dollars against it for a real-world need, then repay and reclaim their asset later.

The catch is the part you must respect. If the value of your collateral falls too far, toward your loan amount, the smart contract will automatically sell it to repay the debt. This is called liquidation, and it happens without warning, mercy, or appeal, because it is just code following its rules. Crypto can fall fast, and people who borrow carelessly against volatile collateral can wake up to find it has been liquidated in a crash.

The machine does exactly what it promised, which is precisely the danger.

The honest ledger of risks

A report that only sold you the freedom would be doing the same dishonest thing the loudest crypto voices do. Becoming your own bank means absorbing risks a bank normally absorbs for you, and you deserve the full list.

The first is the one we have stressed: you are responsible for your keys. Lose them or expose them, and the money is gone with no recourse. This single fact causes enormous, permanent losses every year.

The second is smart-contract risk. A smart contract is only as good as its code, and code can have flaws. Attackers hunt for those flaws, and when they find one in a protocol holding deposits, they can drain it. The sums lost to such exploits run into the billions of dollars a year, and even well-regarded protocols have been hit. Putting money into a protocol means trusting its code the way you would once have trusted a bank's solvency.

The third is stablecoin risk. A stablecoin is only as reliable as whatever backs it. Most of the time the big ones hold their dollar value, but a stablecoin can depeg, slipping below its intended dollar, especially under stress. If the digital dollar you are holding or borrowing wobbles, it can trigger losses and liquidations.

The fourth is liquidation risk, already described: borrow against volatile collateral and a sharp drop can wipe out your position automatically.

And there is a broader lesson from recent history worth holding onto. Both the centralized crypto lenders that collapsed a few years ago and the decentralized protocols that have been exploited since taught the same thing in different ways: high returns in crypto have repeatedly come with the risk of total loss, and your own bank means there is often no deposit insurance, no regulator, and no one to make you whole. The freedom is real, and so is the exposure.

How to think about this for yourself, for free

This is the part you can act on the moment you finish reading. You do not need to deposit anything to learn, and most of these tools are free.

1. Learn the keys before you risk a cent.

The single most important skill is understanding and safely managing a private key, before any money is involved. Plenty of free, reputable guides explain how wallets and keys work. A neutral starting point is a free explainer like the one at Ethereum.org's guide to wallets. What to look for: complete comfort with how keys work, and a sober respect for the fact that losing them is permanent.

2. Watch the real scale and the real rates.

Independent data tools show how much money sits in DeFi and what protocols actually pay, free of any platform's marketing. A widely used free resource is DefiLlama, which tracks deposits and yields across the ecosystem. What to look for: the genuine size of the system, and yields grounded in real activity rather than eye-watering advertised numbers.

3. Separate the freedom from the responsibility.

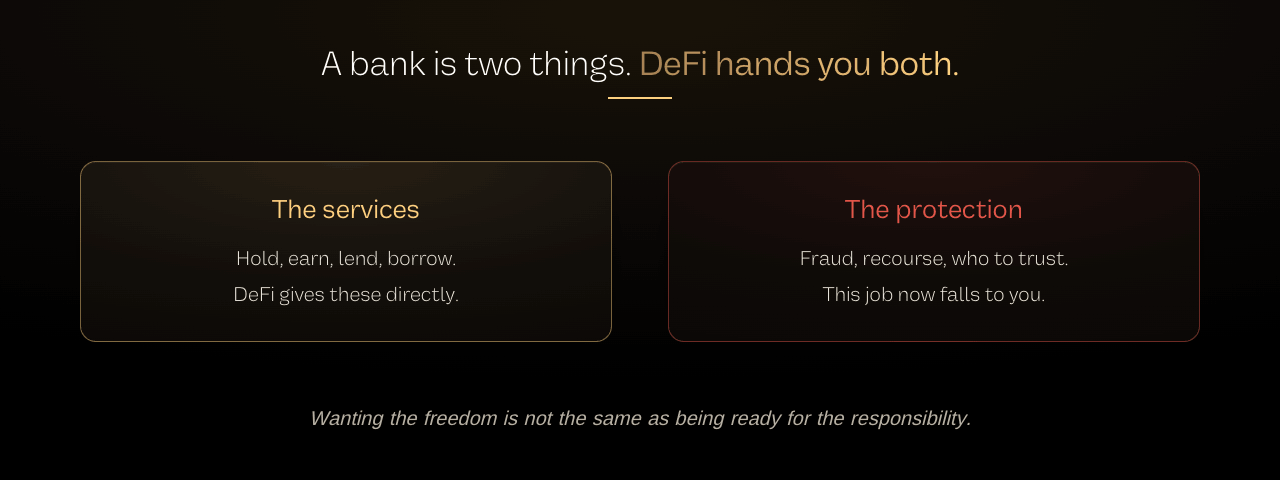

For every benefit DeFi offers, ask what protective job a bank used to do that now falls to you. No frozen accounts, but also no fraud department. No permission needed, but also no one to reverse a mistake. What to look for: an honest personal answer to whether you want that responsibility, because wanting the freedom is not the same as being ready for the burden.

4. Start with understanding, not deposits.

The space rewards patience and punishes haste. The people who lose the most are usually those who rushed in chasing a return before they understood keys, liquidation, and smart-contract risk. What to look for: real understanding first; any decision about actual money comes much later, and only with what you could afford to lose entirely.

A note on expectations, so you use this well. Understanding how to become your own bank does not make doing so safe or right for everyone. For many people, the convenience and protections of a traditional bank are exactly what they want, and that is a perfectly sensible choice. The goal here is to understand what the alternative genuinely is, both the control it offers and the responsibility it demands, so that any choice you make is an informed one.

The one idea to take with you

If you forget everything else, keep this.

A bank is a bundle of two things: services, and protection. It holds and grows and lends your money, and it also absorbs the risks, the fraud, the lost passwords, the question of who to trust.

Become your own bank hands you the services directly, running on open code with no middleman, no permission, and no closing time. That is a genuine and remarkable freedom.

But it hands you the protection job too. You become the keeper of the keys, the fraud department, and the final backstop, with no one to call when something goes wrong. The technology does exactly what it promises, which is the whole appeal and the whole danger at once.

Understanding both halves is what separates the people who use these tools wisely from the people who become cautionary tales. You can learn the entire picture for free, long before any money is involved, which is exactly where anyone sensible begins.

- Rami Al-Sabeq (Editor in Chief | Future Finance)

About Future Finance

Future Finance is written by Rami Al-Sabeq, Editor-in-Chief, and his research team. His macro-to-crypto work has been featured in Unchained and Cryptonary, and his independent essays appear at RamiWrites.Substack.com.

Behind every issue sits Head of Research Tyler Hubbard, whose track record across 590+ digital asset picks has produced an 85% directional accuracy rate and a 426% average peak return. That's as of the third-party audit measuring performance through April 30th, 2026. Follow him on TradingView here.

Editor's Pick

Become a sharper capital allocator in 5 minutes a day.

Institutional-grade research on where the smartest capital is positioning, across AI, energy, biotech, robotics, and digital assets. Distilled into a daily read you finish before your coffee does.

Join 45,000+ readers · No spam · Unsubscribe anytime