One Product Paid 40% a Year. Now It Pays 3.5%. Here's What Changed.

How to tell durable crypto income from the kind that quietly evaporates

4 min red

The briefing serious investors read first.

Free analysis before markets open. Start thinking in decades, not days.

Join 45,000+ readers · No spam · Unsubscribe anytime

Before we begin: this report is for education, not financial advice. Nothing here is a recommendation to buy or sell any stock, company, or asset, and we make no price predictions. Investing carries risk, including loss. Please read the full disclaimer at the end.

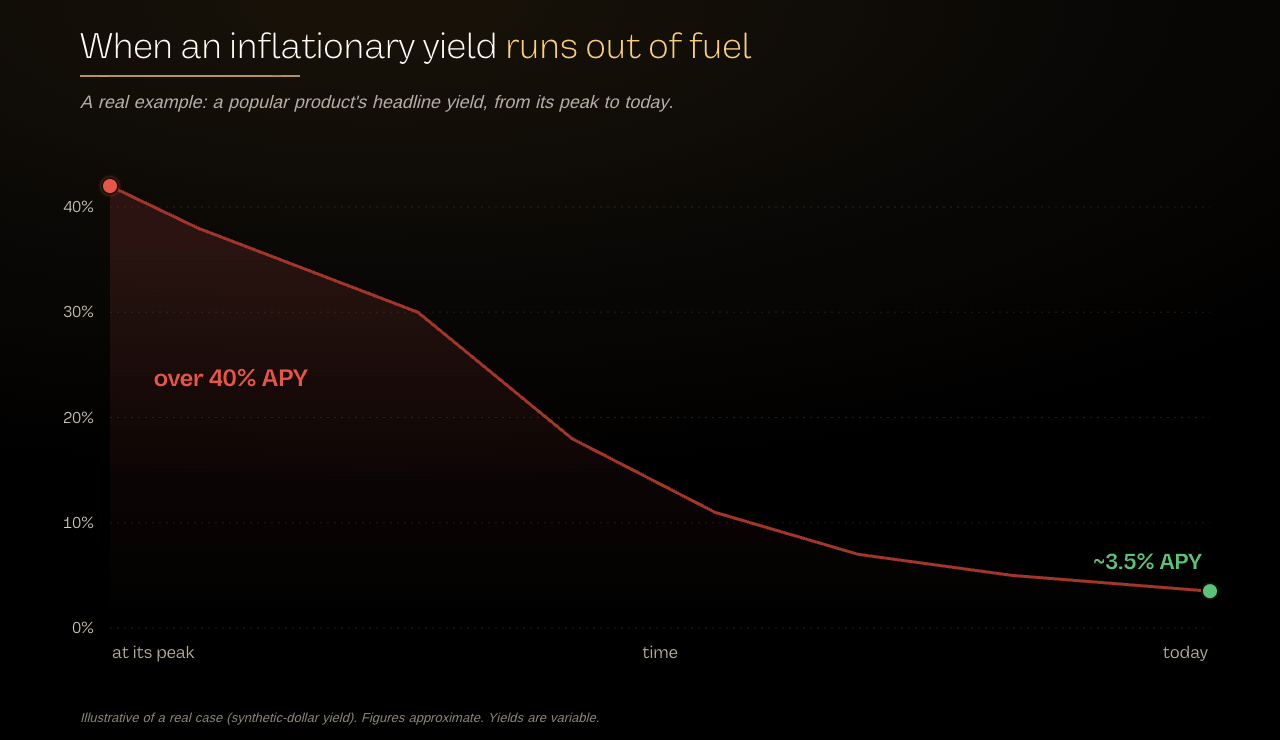

The 40% that turned into 3%

A couple of years ago, parts of the crypto world were advertising returns that sounded too good to be true. One popular product offered more than 40% a year on what was effectively a digital dollar. Billions of dollars poured in.

Today that same product pays closer to 3.5%, and most of the money that chased the big number has left.

That collapse is not a scandal or a hack. It is the single most important lesson in earning yield on crypto, playing out in public. The 40% was never what most assumed it to be, and the people who understood why kept their composure while everyone else learned the hard way.

But here's what everyone is missing in the headlines...

There are two completely different kinds of yield in crypto, and they look identical on the screen. One is durable, paid out of real economic activity. The other is a temporary incentive, conjured out of thin air to attract you, and destined to shrink. Telling them apart is the most valuable skill a crypto saver can develop, and almost nobody teaches it plainly. This report does. None of it is a recommendation to chase any return. It is a way of thinking that helps you understand what you are actually being paid, and why.

What yield even means here

Let us start from the ground, because the jargon hides a simple idea.

Yield is just the return you earn for putting your money to work, usually expressed as a percentage per year. A savings account that pays 4% a year is offering a 4% yield.

The crypto world borrows the same word for the returns you can earn by depositing your coins into various services. You will see it written as APY, which stands for annual percentage yield. It is simply the rate, including the effect of compounding, that you would earn over a year.

When a crypto platform advertises 8% APY, it is promising, or appearing to promise, an 8% return over twelve months.

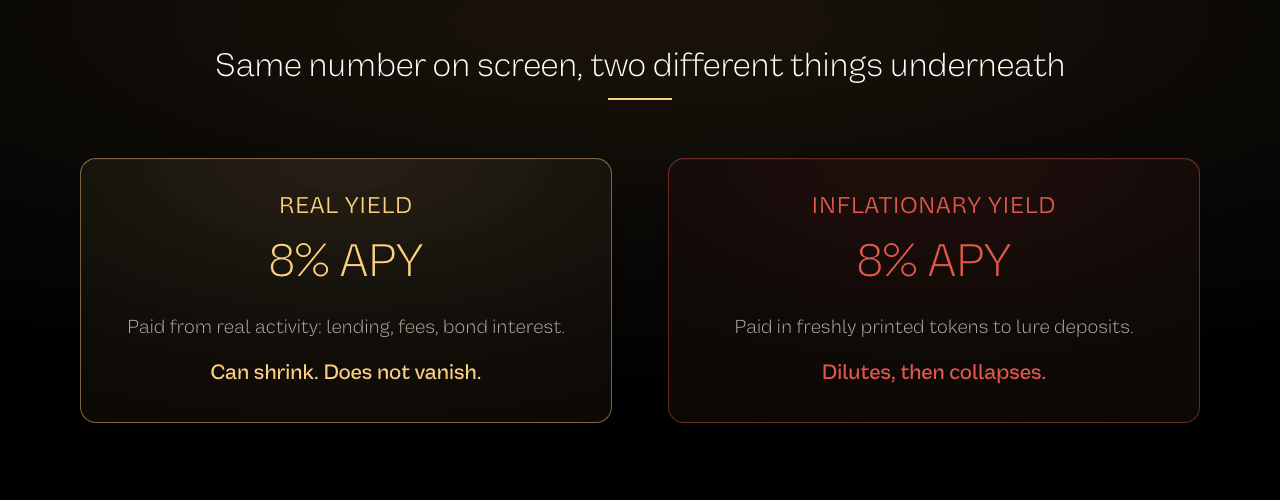

The trouble is that two platforms can both flash 8% APY on the screen while paying you in two completely different ways, with completely different odds of that number surviving. One is real. The other is, in a sense, borrowed from the future. Understanding the difference starts with asking one question.

The one question that explains everything: where does the money come from?

Whenever you are offered a yield, the only question that truly matters is this. Who is actually paying me, and why?

There are only a few honest answers, and a few dishonest ones. Sorting them is the whole game.

A yield is real when the money paid to you comes from genuine economic activity. Someone, somewhere, is doing something productive and sharing the proceeds with you. The payment has a source that can last.

A yield is inflationary when the money paid to you is mostly freshly created tokens, printed by the project itself to lure deposits. There is no productive activity underneath. The project is simply handing out more of its own coins, and that generosity dilutes the value of every coin in existence, including the ones you are being paid with.

The names come from that distinction. Real yield is paid out of real revenue. Inflationary yield is paid by inflating the token supply. On the screen, both might say 20% APY. Underneath, one is a salary and the other is a printing press.

ABN System

Spotting real yield is step one. Earning it safely is the system.

Knowing durable income from a temporary bribe is the foundation. Putting it to work without taking on reckless risk is the skill. Our free ABN System training walks through the exact three-part framework we use to generate real, sustainable yield.

Watch the ABN System training →Where real yield actually comes from

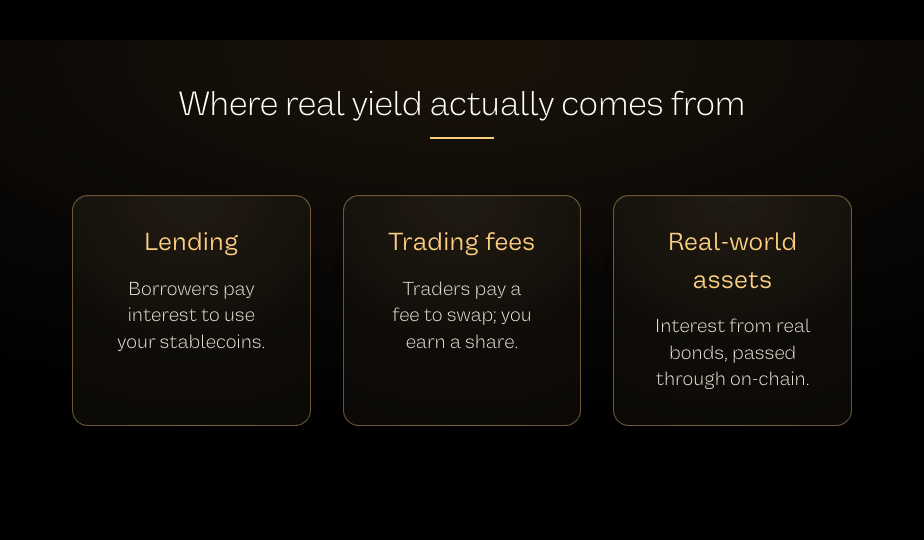

It helps to know the legitimate sources, because they are not mysterious. In crypto, durable yield mostly comes from a handful of genuine activities.

The first is lending. When you deposit a stablecoin into a lending service, other people borrow it and pay interest. That interest, minus a cut for the platform, flows to you.

As long as real borrowers want to borrow, the yield has a real source. It rises when borrowing demand is high and falls when it is low, exactly as you would expect from honest interest.

The second is trading fees. Some services let you supply your coins to a pool that traders use to swap one asset for another. Every trade pays a small fee, and a share of those fees goes to the people who supplied the pool.

When trading is busy, the fees are meaningful. The income is real because real traders are really paying it.

The third, and increasingly important, is real-world assets. A growing share of the most reliable crypto yield now comes from tokenized versions of safe, traditional investments, most notably US government bonds.

The yield is the interest those bonds pay in the offline world, passed through to you on-chain. It is about as real as yield gets, because its source is the same thing that pays a traditional bond investor.

Notice the common thread. In every case, somebody is genuinely paying for something, borrowing money, trading, or issuing debt, and you are receiving a slice of that genuine payment. The yield can shrink, but it does not simply vanish, because it was never an illusion.

Where inflationary yield comes from, and why it always fades

Now the other kind.

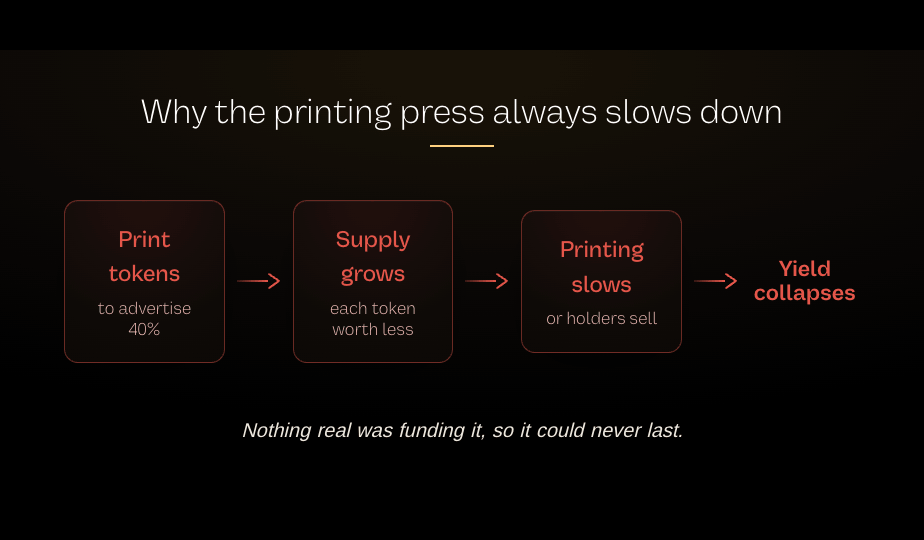

Imagine a brand-new project that wants to attract deposits quickly. It does not yet have real borrowers or busy trading or bonds throwing off interest. So it does the one thing it easily can: it prints its own brand-new token and pays that out as a reward.

For a while, the advertised number can be enormous. Forty percent. A hundred percent. Sometimes more.

The project is effectively buying your attention with freshly minted coins, and the eye-watering rate pulls in a flood of deposits.

Here is the catch that the big number hides. Every new token printed makes each existing token a little less scarce, and therefore a little less valuable.

You might be earning a 40% return measured in those tokens while the tokens themselves quietly lose value underneath you. It is a bit like being paid a soaring salary in a currency that is being printed into worthlessness. The headline figure soars; the real value drifts away.

And it cannot last, because nothing real is funding it. Once the project slows the printing, or once enough people try to sell their rewards at the same time, the advertised yield collapses and the token often falls with it.

The 40% that became 3.5% was this exact story. The incentives were never paid out of real activity. They were paid out of a printing press that eventually had to slow down.

This is why inflationary yield is sometimes called mercenary. It rents your capital with an unsustainable bribe, and the moment the bribe shrinks, the capital leaves.

The honest state of things right now

This is where intellectual honesty matters more than salesmanship, especially today.

Crypto yields have fallen dramatically from the heady numbers of a couple of years ago. The easy, enormous returns are largely gone. On the most reputable lending services, a stablecoin might earn somewhere in the low-to-mid single digits, and at times that has actually dipped below what a plain traditional savings account or a government bond pays.

That is the opposite of the pitch crypto usually makes. There have recently been stretches where you could take on all the genuine risks of DeFi, smart-contract bugs, platform failure, the chance of losing everything, and be paid less than you would earn risk-free in a bank or a Treasury. When that is true, the extra risk is not being rewarded at all.

Why have yields fallen so far? Partly because the era of reckless token printing has cooled. Partly because large, professional money has flowed in, and more supply of capital chasing the same borrowers naturally pushes rates down, the same dynamic you would see anywhere.

The market has matured, and mature markets pay more modest, more honest returns.

This is not a reason to dismiss crypto yield. It is a reason to judge it soberly. In today's environment, a real yield of a few percent from a genuine source can be perfectly sensible for someone who understands the risks. An advertised yield far above what the real economy is paying should make you more suspicious, not more excited. When a number looks too good in a low-yield world, the most likely explanation is that it is the inflationary kind, and you are early to a party that ends badly.

Gems Uncovered

Honest yields are modest now. We find the real ones.

In a market where the easy returns are gone, separating genuine yield from inflationary bait matters more than ever. Gems Uncovered is our premium letter that surfaces high-conviction opportunities each week, with the real source of every yield laid out plainly.

See how Gems Uncovered works →The risks that apply to all of it

Even real yield is not safe yield. This deserves saying plainly, because it is where people get hurt.

When you deposit money into any crypto protocol, you are trusting computer code to behave exactly as promised. That code can have bugs, and it can be attacked. The amount of money stolen through such exploits runs into the billions of dollars a year. A genuine, real-yield platform can still be drained by a clever attacker, and if it is, your deposit can vanish regardless of how honest the yield was.

There are other hazards too. The stablecoin you deposit could lose its intended value. The platform could fail or freeze withdrawals. The rules can change. None of these risks disappear just because a yield is real rather than inflationary.

So the real-versus-inflationary distinction is necessary, but it is not sufficient. It tells you whether a yield can last. It does not tell you whether the platform is safe. Both questions matter, and a sensible person asks both before depositing a single coin.

How to judge a yield yourself, for free

This is the part you can act on the moment you finish reading. Most of the tools below are free to use.

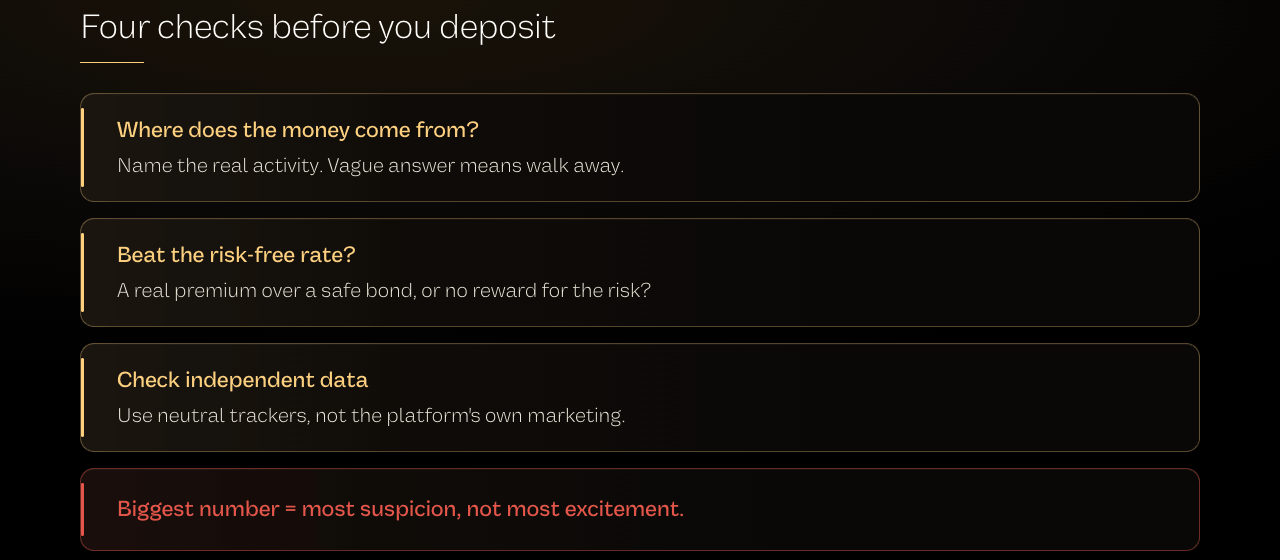

1. Always ask where the money comes from.

Before you deposit anywhere, find the answer to one question: what activity is paying this yield? If the platform can clearly point to lending interest, trading fees, or bond income, that is a real source. If the answer is vague, or if the rewards are mostly the platform's own token, treat the number with deep suspicion. What to look for: a clear, real-economy source you can actually name.

2. Compare the yield to the risk-free rate.

Hold any crypto yield up against what a safe government bond pays right now, the risk-free rate from our other report. If a crypto product pays only a little more, or even less, than the risk-free rate, you are being poorly paid for serious extra risk. What to look for: a real premium over the safe rate that genuinely compensates for the danger. No premium is a red flag.

3. Use free data tools to see the real numbers.

Independent sites track actual yields and how much money is deposited across DeFi, rather than relying on a platform's own marketing. A widely used free resource is DefiLlama, which lists yields and total deposits across protocols. What to look for: yields that are stable and backed by real activity, and be wary of sky-high rates attached to tiny or brand-new projects.

4. Be most skeptical when the number is biggest.

This is the counterintuitive habit that protects you. In a world where honest yields are modest, the highest advertised returns are usually the least sustainable. The eye-watering APY is a warning label, not a prize. What to look for: treat any return far above the real economy's going rate as inflationary until proven otherwise.

A note on expectations, so you use this well. Understanding real versus inflationary yield does not make any deposit safe, and it will not find you a magic high return, because in today's market those mostly do not exist honestly. What it does is stop you from mistaking a temporary bribe for durable income, which is the mistake that has cost crypto savers the most.

The one idea to take with you

If you forget everything else, keep this.

When you are offered a yield, ask who is paying you and why. If the answer is real activity, lending, trading, or bond interest, the yield has a chance of lasting. If the answer is a project printing its own token to lure you in, the number will shrink, and you do not want to be the last one holding the rewards when it does.

In a world where honest returns have become modest, the biggest advertised yields are usually the emptiest. The skill is not finding the highest number. It is understanding what any number is actually made of, and judging whether the risk you take is being honestly paid.

You can ask that question for free, before you deposit a single coin. Most people never ask it at all, which is exactly why the 40% always finds new believers.

- Rami Al-Sabeq (Editor in Chief | Future Finance)

About Future Finance

Future Finance is written by Rami Al-Sabeq, Editor-in-Chief, and his research team. His macro-to-crypto work has been featured in Unchained and Cryptonary, and his independent essays appear at RamiWrites.Substack.com.

Behind every issue sits Head of Research Tyler Hubbard, whose track record across 590+ digital asset picks has produced an 85% directional accuracy rate and a 426% average peak return. That's as of the third-party audit measuring performance through April 30th, 2026. Follow him on TradingView here.

Free Strategy Call

Where to go from here

The right yield for you depends on the risk you can carry. Understanding real versus inflationary yield is the lens. Applying it to your money, your goals, and your tolerance for the very real risks of DeFi is the harder part. On a free strategy call, we'll talk it through, no jargon, no obligation.

Book your free strategy call →Disclaimer: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. Future Finance is not a registered financial advisor or broker-dealer. The data sources and tools referenced are provided for independent research and are not endorsements. Decentralized finance and cryptocurrency are highly volatile and carry severe risks, including smart-contract exploits, platform failure, stablecoin depegs, and the total loss of deposited funds; protocols named or alluded to are illustrative examples only and are not recommendations. All yields are variable and not guaranteed, and past or advertised returns are not indicative of future results. The figures cited are approximate and accurate only as of mid-2026; they change constantly, so verify all current data independently using the linked sources. Markets can move against you, and you should never deposit money you cannot afford to lose. Always conduct your own research and consult a qualified, licensed financial advisor who understands your personal circumstances before making any financial decision.

Editor's Pick

Become a sharper capital allocator in 5 minutes a day.

Institutional-grade research on where the smartest capital is positioning, across AI, energy, biotech, robotics, and digital assets. Distilled into a daily read you finish before your coffee does.

Join 45,000+ readers · No spam · Unsubscribe anytime