One Boring 4% Number Quietly Prices Every Investment You Own

Why the boring bond market quietly decides what every other investment is worth

5 min read

The briefing serious investors read first.

Free analysis before markets open. Start thinking in decades, not days.

Join 45,000+ readers · No spam · Unsubscribe anytime

Before we begin: this report is for education, not financial advice. Nothing here is a recommendation to buy or sell any stock, company, or asset, and we make no price predictions. Investing carries risk, including loss. Please read the full disclaimer at the end.

The most important number nobody talks about

Let us start with a confession most people in finance will never make out loud.

The flashiest assets get all the attention. The hot stock. The coin that tripled. The property deal your cousin will not stop talking about.

Meanwhile, the single most powerful number in all of investing sits in a corner, wearing a gray suit, being ignored.

It is the yield on a government bond.

And once you understand what it does, you will never look at your portfolio the same way again.

Here is the short version, and we will unpack every piece of it. A government bond yield is what the financial world calls the risk-free rate. It is the return you can earn while taking almost no risk at all. And because it exists, every other investment on Earth, your stocks, your gold, your crypto, your rental property, has to compete with it.

But here's what everyone is missing in the headlines…

When that boring number rises, it quietly raises the bar that every exciting investment has to clear. Assets can fall even when nothing went wrong with them. The safe alternative simply got more tempting. Miss this, and the market looks random. See it, and a lot of things suddenly make sense.

First, what even is a bond?

Let us build this from the ground up, because almost nobody is taught it properly.

Imagine your friend asks to borrow money. You agree to lend it, on the condition that they pay you a little interest each year, and hand back the full amount on an agreed date.

That is a bond. You are the lender. They are the borrower. The interest is your reward, and the agreed payback date is called the maturity.

When a government wants to borrow, it does the exact same thing, except instead of borrowing from one friend, it borrows from millions of investors around the world. A 10-year Treasury bond is simply a loan to the US government that gets paid back in 10 years, with interest along the way.

The return you lock in when you make that loan has a name. It is called the yield.

So far, so simple. Now here is the one twist that trips up almost everyone.

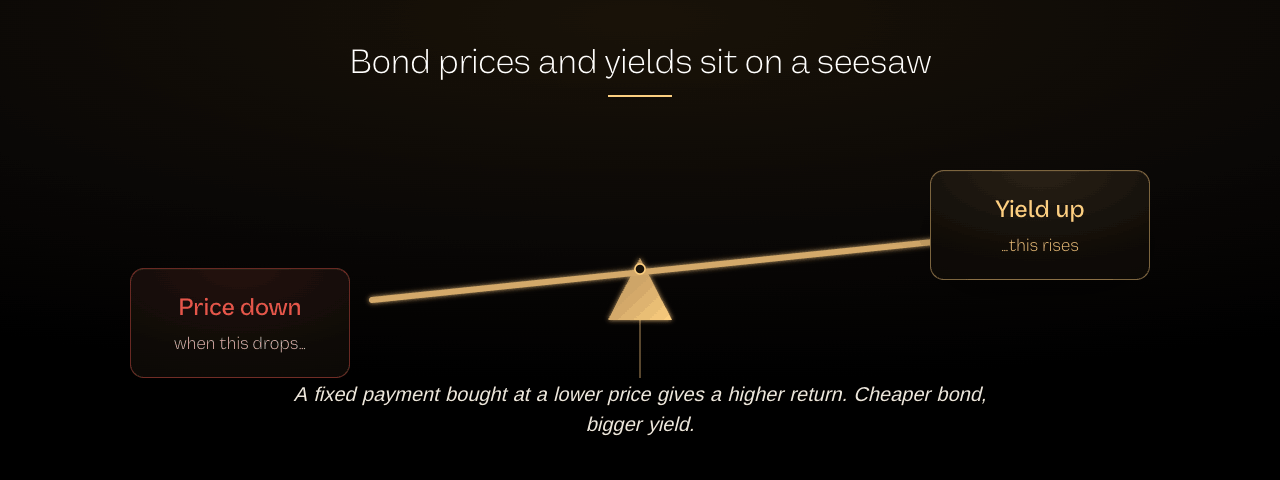

The twist: prices and yields move in opposite directions

This is the single most counterintuitive thing about bonds, and it is worth slowing down for.

When investors do not want bonds, their prices fall, and the yield rises. When investors love bonds, prices rise, and the yield falls.

Think of it like this. A bond pays a fixed dollar amount. If you can buy that same fixed payment for a lower price, then your return on what you paid is higher. Cheaper bond, bigger yield. More expensive bond, smaller yield. They are two ends of the same seesaw.

So the next time you see a headline shouting that "yields are rising," translate it in your head. It means the market is demanding a bigger reward to lend money. Often that is the market saying it is nervous, or that it expects inflation, or that it simply has better things to do with its cash.

That single translation already puts you ahead of most people reading the same headline.

Why this one number rules them all

Now for the part that ties everything together.

US Treasury bonds are considered the safest investment on the planet. The US government has never missed a payment, and it can, in the last resort, create the dollars it owes. So lending to it is about as close to "no risk" as the financial world believes exists.

That is why the yield on a Treasury is called the risk-free rate. It is the return you can get without taking any meaningful risk at all.

And here is the magic. Every other asset on Earth gets measured against it.

If a 10-year Treasury pays you a guaranteed return, then gold, stocks, real estate, and Bitcoin all have to offer you more than that to be worth the extra risk. Why would you accept the wild swings of a risky asset for the same return you could lock in safely?

That comparison runs in the head of every serious investor, every single day. The risk-free rate is the hurdle. It is the bar that everything else has to jump over.

When the bar is low, almost everything clears it, and money flows happily into riskier, higher-returning assets. When the bar rises, fewer things clear it, and money starts rotating back toward safety.

ABN System

Now you know the hurdle. Here's how to clear it.

The risk-free rate sets the bar. Building a portfolio that genuinely clears it, without taking reckless risk or chasing yield that does not deserve to be trusted, is the system. Our free ABN System training walks through exactly how we do that.

Watch the ABN System training →The pension fund thought experiment

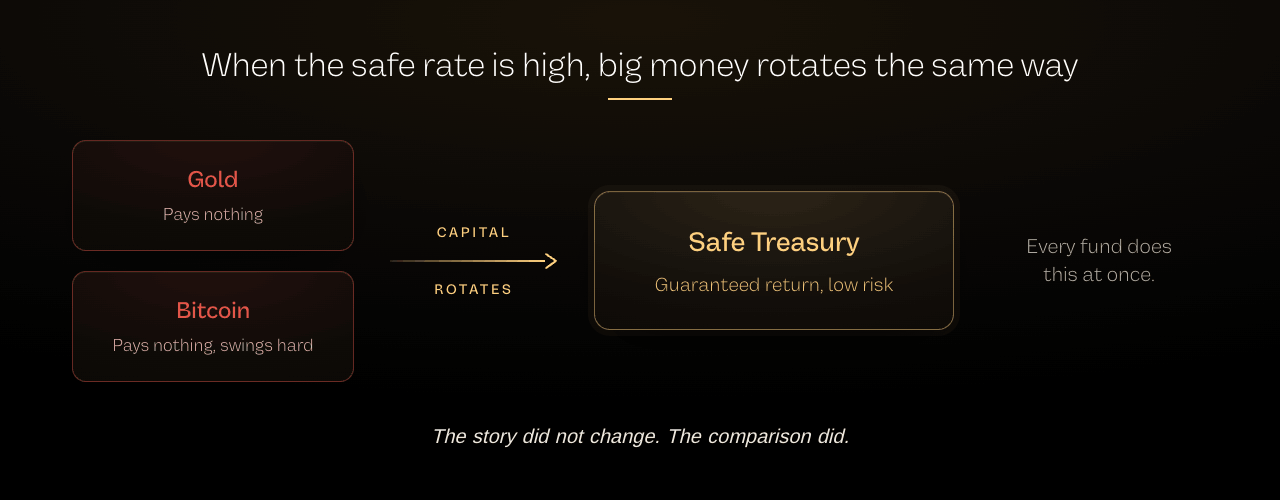

Let us make this real with a story.

Picture a pension fund manager. Call her Sarah. She is responsible for billions of dollars that millions of future retirees are counting on. Her job is not to gamble. Her job is to not lose.

Sarah has a choice in front of her.

She can buy a 10-year Treasury and lock in a guaranteed return with effectively zero risk.

Or she can hold gold, which pays her nothing and has been choppy.

Or she can hold Bitcoin, which pays her nothing either and can swing wildly in a week.

When that guaranteed Treasury return is high enough, which do you think Sarah chooses?

She rotates into bonds. And she is not the only one. Every institution like hers runs the same math at the same time. Insurance companies, sovereign wealth funds, retirement plans, all of them tilt toward the safe, guaranteed return at once.

That synchronized rotation is a quiet tidal force. It is why gold can drift sideways and crypto can sag even when nothing about their underlying stories has changed.

The story did not change. The comparison did.

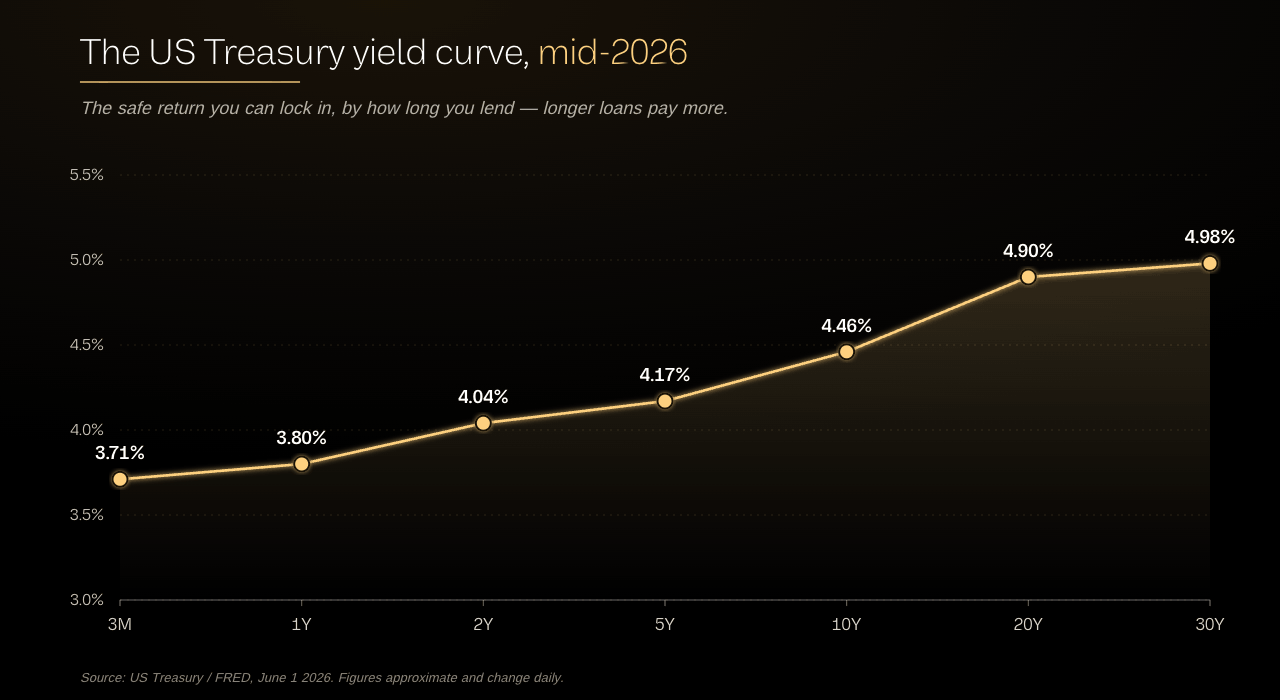

Where rates stand as you read this

To make this concrete, here is a snapshot of the US Treasury yield curve from mid-2026. These move every single day, so treat them as a starting point and check the live links later in this report.

A "yield curve" is just the set of yields across different loan lengths, from very short to very long, lined up side by side. Normally, longer loans pay more, because lending for 30 years is riskier than lending for three months.

As of this snapshot, that is roughly what we see: short-term yields sit lower, and the reward climbs as you lend for longer, out to a 30-year bond paying around 5%.

When long-term yields sit near 5%, the bar for every risky asset is high. That is the environment a lot of investors have been navigating, and it explains a good deal of why risk assets have had to fight for every gain.

There is one more wrinkle worth knowing. Sometimes the curve gets strange, and very long loans pay about the same as, or even less than, slightly shorter ones. When that happens, it is a sign the bond market is stressed or expecting trouble, and it is worth paying attention to. And this is not only a US story. Long-term government yields have been elevated across the UK, Japan, and other major economies too. The tide is global.

The lesson history keeps teaching

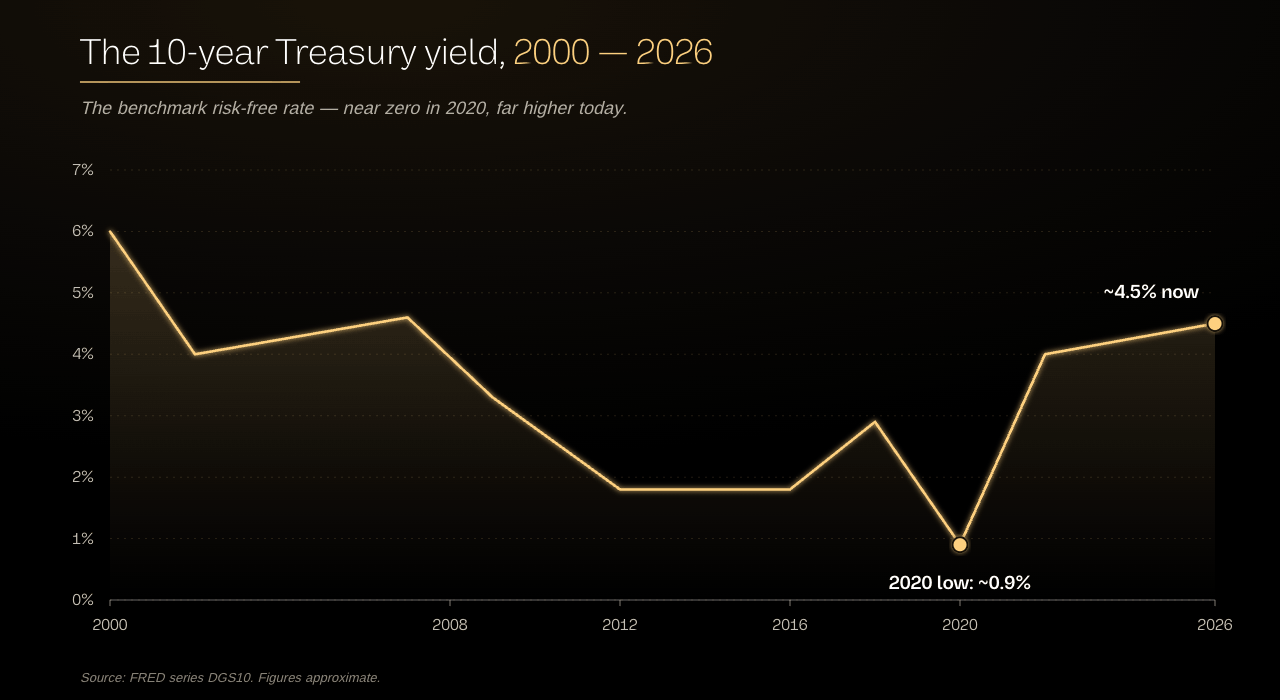

If this still feels abstract, history has a blunt reminder.

Back in 2018, the risk-free rate climbed as the US central bank pushed rates up. Yields that would look modest today were suddenly high enough to tempt money away from risk. Risky assets sold off hard. They had not broken. For the first time in years, capital simply had a safe and decent alternative.

The assets did not get worse. The competition got better. That is the whole mechanism in one sentence.

And it cuts both ways. When the risk-free rate eventually falls, the bar drops, safe returns get less tempting, and money tends to rotate back out toward risk in search of something better. Investors who understand the seesaw can see that shift coming before the headlines announce it.

Gems Uncovered

The hurdle moves. We track what clears it.

When the risk-free rate shifts, the relative value of everything else shifts with it. Gems Uncovered is our premium letter that surfaces high-conviction ideas each week, evaluated against what the current hurdle actually demands in real return and real risk.

See how Gems Uncovered works →How to watch the risk-free rate yourself, for free

This is the part you can act on the moment you finish reading. All of this data is public and free.

1. Check the 10-year Treasury yield.

This is the single most-watched number in global finance, the benchmark risk-free rate everything else is measured against. The Federal Reserve Bank of St. Louis publishes it free on its FRED database.

Open the 10-year Treasury yield chart on FRED.

What to look for: the direction. A rising 10-year means the bar for risky assets is climbing. A falling one means it is dropping.

2. Look at the whole yield curve.

Seeing every maturity at once, from three months to 30 years, tells you what the bond market expects. The US Treasury publishes the full curve every business day.

See the daily Treasury yield curve direct from the source.

What to look for: is the curve sloping up normally, or has it gone flat or strange? A stressed curve is a signal worth respecting.

3. Compare the short end and the long end.

The gap between a short-term yield and a long-term one, often the 2-year against the 10-year, is one of the most-watched signals in markets. The two source series are free on FRED.

The 2-year and the 30-year Treasury yields.

What to look for: when the short end rises above the long end, history says it is worth paying attention.

4. Ask the simple question.

Whenever you are weighing a risky investment, run Sarah's math. What is the guaranteed return on a safe Treasury right now, and is the risky asset offering enough extra to justify its risk? You do not need a finance degree to ask it. You just need to know the risk-free rate, which you can now find in seconds.

A note on expectations, so you use this well. The risk-free rate is a powerful lens, not a crystal ball. It tells you which way the gravity is pulling on risk assets, not exactly when or how far any single one will move. Use it to understand the environment, not to time the next hour.

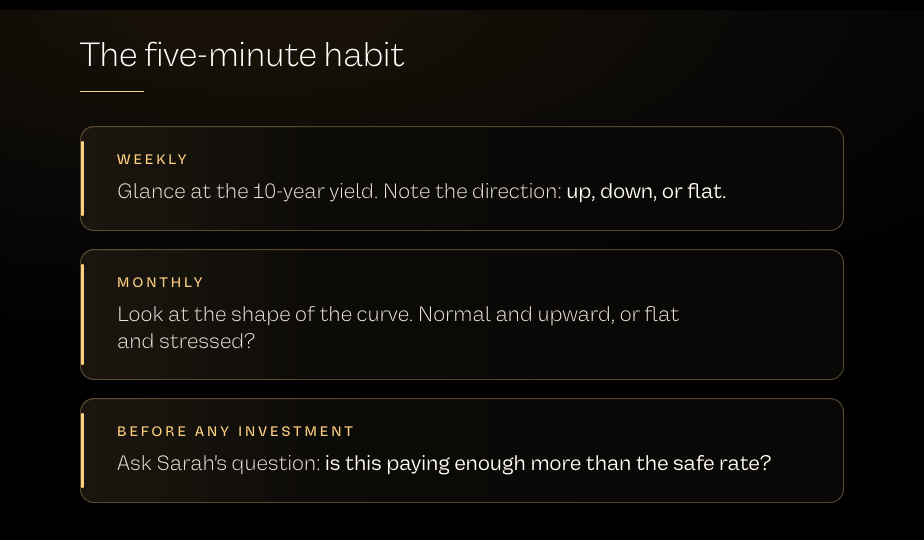

The five-minute habit

You do not need to watch this all day. A light, regular check keeps you oriented.

Once a week, glance at the 10-year yield and note the direction. Up, down, or flat.

Once a month, look at the shape of the whole curve. Normal and upward-sloping, or flat and stressed?

Whenever you size up a new investment, ask Sarah's question: is this risky asset paying me enough more than the safe rate to be worth it?

That is the entire habit. The direction, the shape, and the comparison. Do it consistently and you will understand the force tugging on your whole portfolio better than most people who trade for a living.

The one idea to take with you

If you forget everything else, keep this.

There is a single safe return sitting in the background of every market, and it sets the price of admission for risk. When it rises, every exciting investment has to work harder to be worth it. When it falls, the leash loosens and money goes looking for adventure again.

It is not the loudest number in the room. It is the most important one. Now you know where to find it, and what it is quietly telling you.

- Rami Al-Sabeq (Editor in Chief | Future Finance)

About Future Finance

Future Finance is written by Rami Al-Sabeq, Editor-in-Chief, and his research team. His macro-to-crypto work has been featured in Unchained and Cryptonary, and his independent essays appear at RamiWrites.Substack.com.

Behind every issue sits Head of Research Tyler Hubbard, whose track record across 590+ digital asset picks has produced an 85% directional accuracy rate and a 426% average peak return. That’s as of the third-party audit measuring performance through April 30th, 2026. Follow him on TradingView here.

Free Strategy Call

Where to go from here

Every investment you own is measured against this bar. Whether your current portfolio actually clears it, and how to adjust if it does not, is a personal conversation. On a free strategy call, we will walk through what that means for your goals and risk tolerance, no jargon, no obligation.

Book your free strategy call →Disclaimer: This report is for educational and informational purposes only and does not constitute financial, investment, legal, or tax advice. Future Finance is not a registered financial advisor or broker-dealer. The data sources and tools referenced are provided for independent research and are not endorsements. All investments carry risk, including the possible loss of the entire amount invested. Bonds themselves carry risks, including interest-rate risk and the effect of inflation on real returns. Past performance is not indicative of future results, and historical patterns described here may not repeat. The financial figures cited are approximate and accurate only as of mid-2026; they change constantly, so verify all current data independently using the linked sources. Markets can move against you, and you should never invest money you cannot afford to lose. Always conduct your own research and consult a qualified, licensed financial advisor who understands your personal circumstances before making any investment decision.

Editor's Pick

Become a sharper capital allocator in 5 minutes a day.

Institutional-grade research on where the smartest capital is positioning, across AI, energy, biotech, robotics, and digital assets. Distilled into a daily read you finish before your coffee does.

Join 45,000+ readers · No spam · Unsubscribe anytime